February 17, 2026 · 5 min read

How Does Polymarket Make Money?

$23 billion in trading volume. Zero dollars in revenue. Not a cent.

That sounds like a broken business, right? But investors have poured billions into Polymarket anyway. So how does Polymarket make money if it doesn't charge anyone to use the platform?

Short answer: it mostly doesn't. Not yet. And I think that's actually the most interesting part of the whole thing. The company is deliberately burning cash to corner the prediction market before flipping the switch on monetization. When you look at what they've got lined up (especially the POLY token and a massive deal with the company behind the NYSE), it starts making a lot more sense.

Let me walk you through it.

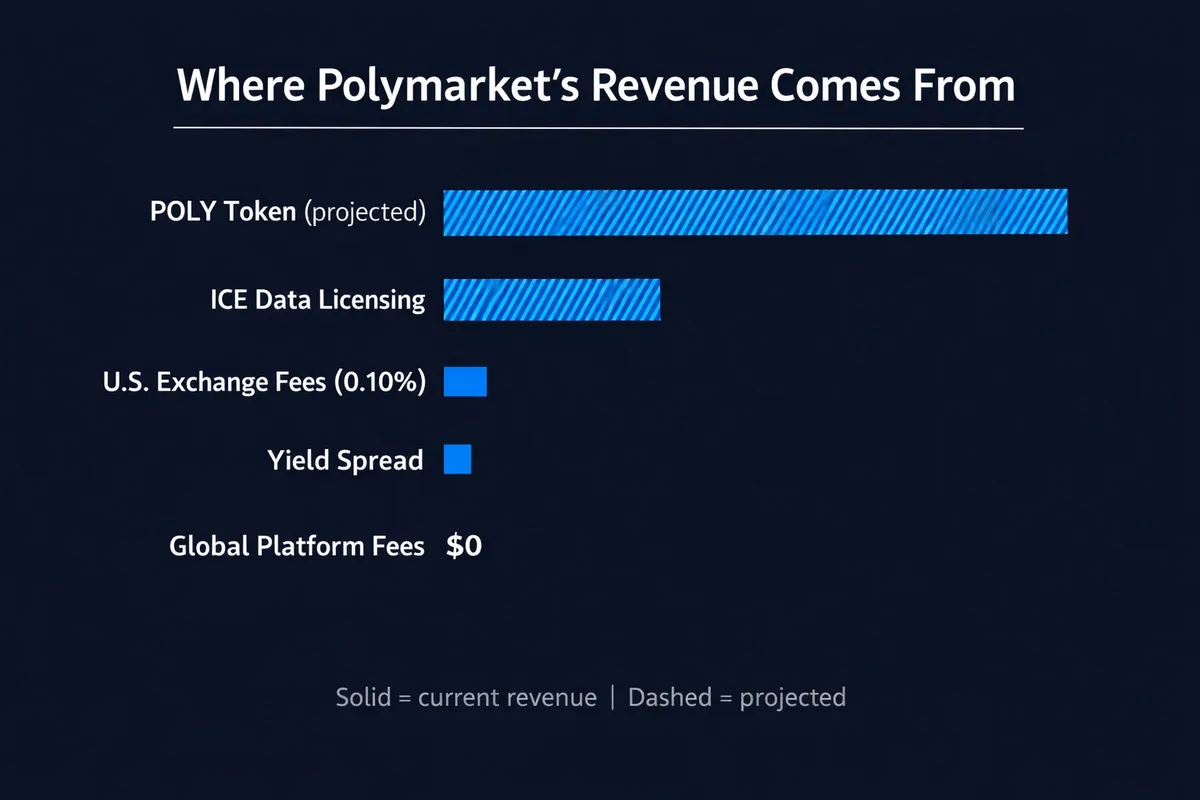

Fees? Barely any.

On the global platform, Polymarket charges zero trading fees. That's been the case since day one.

The one exception is the U.S. exchange. Polymarket spent $112 million buying QCEX, a CFTC-licensed clearinghouse, to re-enter the American market in late 2025. U.S. users now pay a 0.10% taker fee on each trade.

How cheap is that? Kalshi, their main competitor, charges around 1.2%. So Polymarket is still absurdly cheaper.

But even at 0.10%, the revenue is basically a rounding error for a company sitting at a $9 billion valuation. Polymarket knows this. They've hinted the rate won't stay this low forever, but right now, getting people in the door matters more than squeezing out fees.

Some short-duration crypto markets also have selective fees. Tiny amounts. Not worth dwelling on.

So where does the real money come from? It starts with a phone call from the New York Stock Exchange.

The ICE deal most people missed

I think this is the most underrated part of the Polymarket story.

In October 2025, Intercontinental Exchange (ICE owns the NYSE, in case you didn't know) invested $2 billion into Polymarket. That alone pushed the valuation to about $9 billion.

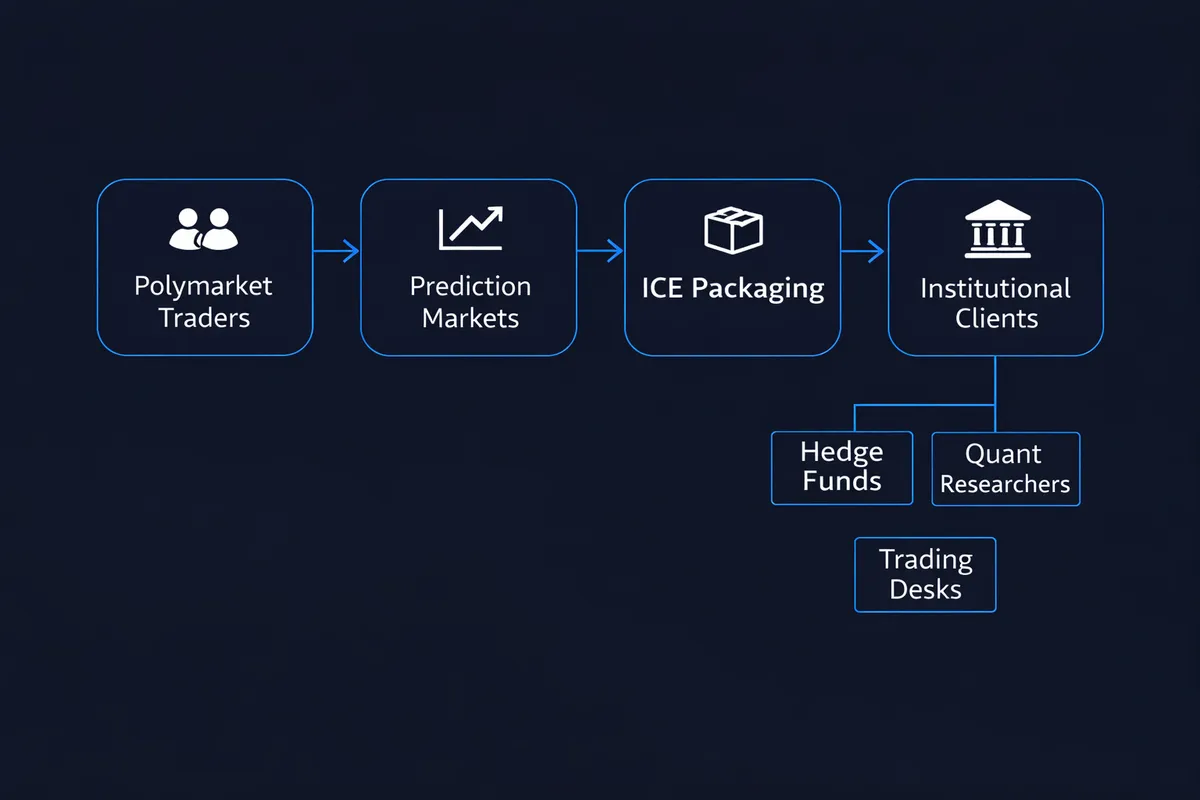

But here's what makes the deal actually interesting. ICE didn't just hand over a check. They're building a data distribution pipeline around Polymarket's markets.

Think about it. Every single market on Polymarket produces real-time probability data. Who wins the election. Whether the Fed cuts rates. Whether a ceasefire holds. Thousands of traders put real money behind these predictions, and the resulting prices tend to be faster and more accurate than traditional polls.

ICE wants to package that data and sell it to Wall Street:

- Real-time probability feeds for trading desks and hedge funds

- Historical data for quant researchers

- API access so firms can plug Polymarket odds into their models

Basically, Polymarket becomes a financial data company. Not a betting app. A data supplier that sits next to Bloomberg and Reuters. And ICE already runs one of the biggest data networks on earth, so the distribution infrastructure is already there.

The revenue split between Polymarket and ICE hasn't been made public. But data licensing? That's a high-margin business. I wouldn't be surprised if this partnership alone ends up being worth hundreds of millions over time.

And it's still not the biggest piece of the puzzle.

The POLY token is where it all comes together

If there's one thing to remember from this article, it's this: the POLY token is how Polymarket plans to actually make money. Everything else is a warmup.

Polymarket's CMO went on the Degenz Live podcast in October 2025 and said it outright. There will be a token. There will be an airdrop. No specific launch date yet, but most people expect sometime in 2026.

What does the token actually do? Three things, based on what's been confirmed and what analysts have pieced together:

- Governance: holders vote on protocol upgrades and platform decisions

- Staking: lock up tokens, earn rewards. Keeps capital glued to the platform

- Fee routing: even a small percentage fee routed through the token becomes real money at Polymarket's volume

And this is the part that makes the math crazy. Analysts speculate around a 0.5% fee. Apply that to $23 billion in annual volume and you get $115 million per year. That's how you justify a $9 to $15 billion valuation.

Revenue Memo's analysis puts it bluntly: token-based fee accrual could eventually make up 90%+ of total revenue. Without the token, Polymarket is a wildly popular platform that makes nothing. With it, the entire business model clicks into place.

One more thing that caught my eye. Early investors reportedly got token warrants, which are essentially options to buy POLY at a discount when it launches. If the people who wrote the biggest checks are betting on the token, that tells you something about where the real value sits.

There's a quieter revenue source, too

Polymarket pays users a 4% annual reward for holding positions in certain long-term markets. Presidential elections, midterms, that kind of thing. It keeps money parked on the platform and keeps those markets liquid.

But that 4% has to come from somewhere, right?

Polymarket earns yield on the pooled deposits in its system. Whatever they make above 4% is profit. It's net interest margin, same thing banks have done forever. Not sexy. But with billions in deposits, even a thin spread adds up.

Why would a $9 billion company charge nothing?

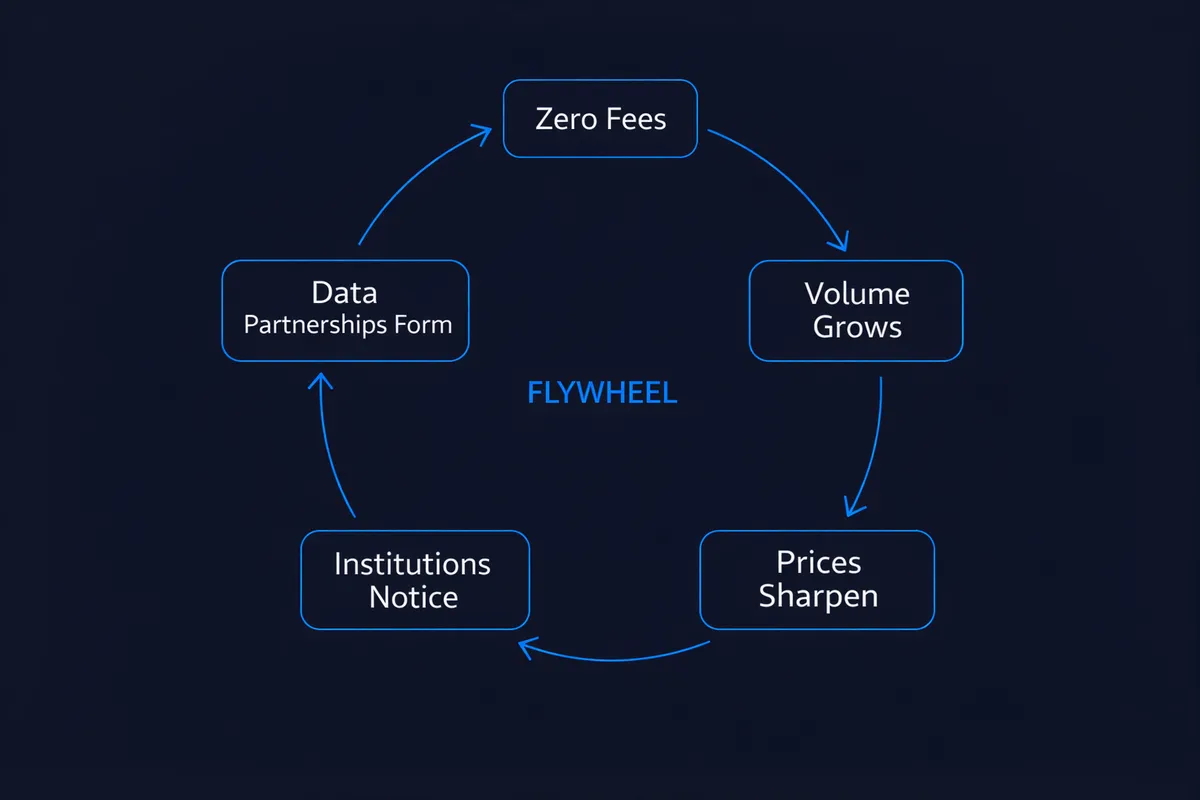

Prediction markets have a brutal cold-start problem. Five traders on a market? Garbage odds. Five thousand? Now you've got prices that rival professional forecasters.

Volume creates accuracy. Accuracy brings more volume. It's a flywheel. But you have to get it spinning first, and fees create friction that slows it down.

So Polymarket killed the fees entirely. Volume exploded. Prices got sharper. Institutions noticed. Media started quoting Polymarket odds in headlines. Data partnerships formed. And now they've got a platform that's incredibly hard to unseat.

You've seen this before. Uber subsidized rides to own the market. Robinhood killed commissions and captured a generation of retail investors.

Same playbook. Dominate first. Charge later.

So is any of this working?

Profitable? No. Not even close.

But look at where they are. $23 billion in volume. $2 billion from the company that runs the NYSE. A token on the way. And U.S. regulators are warming up to prediction markets under CFTC oversight instead of trying to shut them down.

The risks are real. Regulation could swing. The token launch could get delayed. A well-funded competitor could show up tomorrow. I'm not going to pretend any of this is guaranteed.

But if Polymarket nails the POLY launch, if ICE data licensing scales, and if the U.S. exchange keeps growing, they go from zero revenue to potentially hundreds of millions in a pretty short window. Whether that happens comes down to execution over the next 12 to 18 months.